How Capital Women’s Care Competes with Competitors (Part 2) – Healthcare Blog

– Healthcare Blog")

Jason Hines

This is part 2 of Jason and Gigasheets' investigation into the contract dispute between Capital's Care vs UnitedHealthCare, where (partially at my request) he expanded the investigation to see other providers in the same market. Expose something! –Matthew Holt

Despite Capital Women’s Care (CWC) fighting the contract terms with United Health, a deeper understanding of the OBGYN market in Maryland reveals a complex competitive landscape where rates vary widely between providers and procedures. By analyzing price transparency data for UnitedHealthCare and Carefirst Bluecross Blueseeld, we can see exactly how each insurer pays for CWC competitors. The result is eye-opening.

Players in European Obgyn Market in Maryland

Our analysis focuses on four European obsessive providers in Maryland who have contracts with United Healthcare and Carefirst. These four practices were chosen as representatives of the broader market as they have published interest rate data with two insurance companies, allowing direct comparisons. However, the OBGYN landscape in Maryland includes dozens of other providers from solo practitioners to hospital-based practices, each with its own negotiated rate that may follow a different model.

The four providers in our analysis include:

- Capital Women's Care – Large exercise at the UHC Dispute Center, with multiple locations in the area

- Experts in Plaza St. Paul (Mercy Medical Center) – Baltimore-based OBGYN practice with established market presence

- Maryland doctor's edge – Women's Health Group has OBGYN services and is now part of Advantia

- Simmonds, Martin & Helmbrecht – Established both European practices

A sample of four popularists provides valuable insights into competitive dynamics among major market participants and helps relevance the CWC-UHC controversy with a broader industry model.

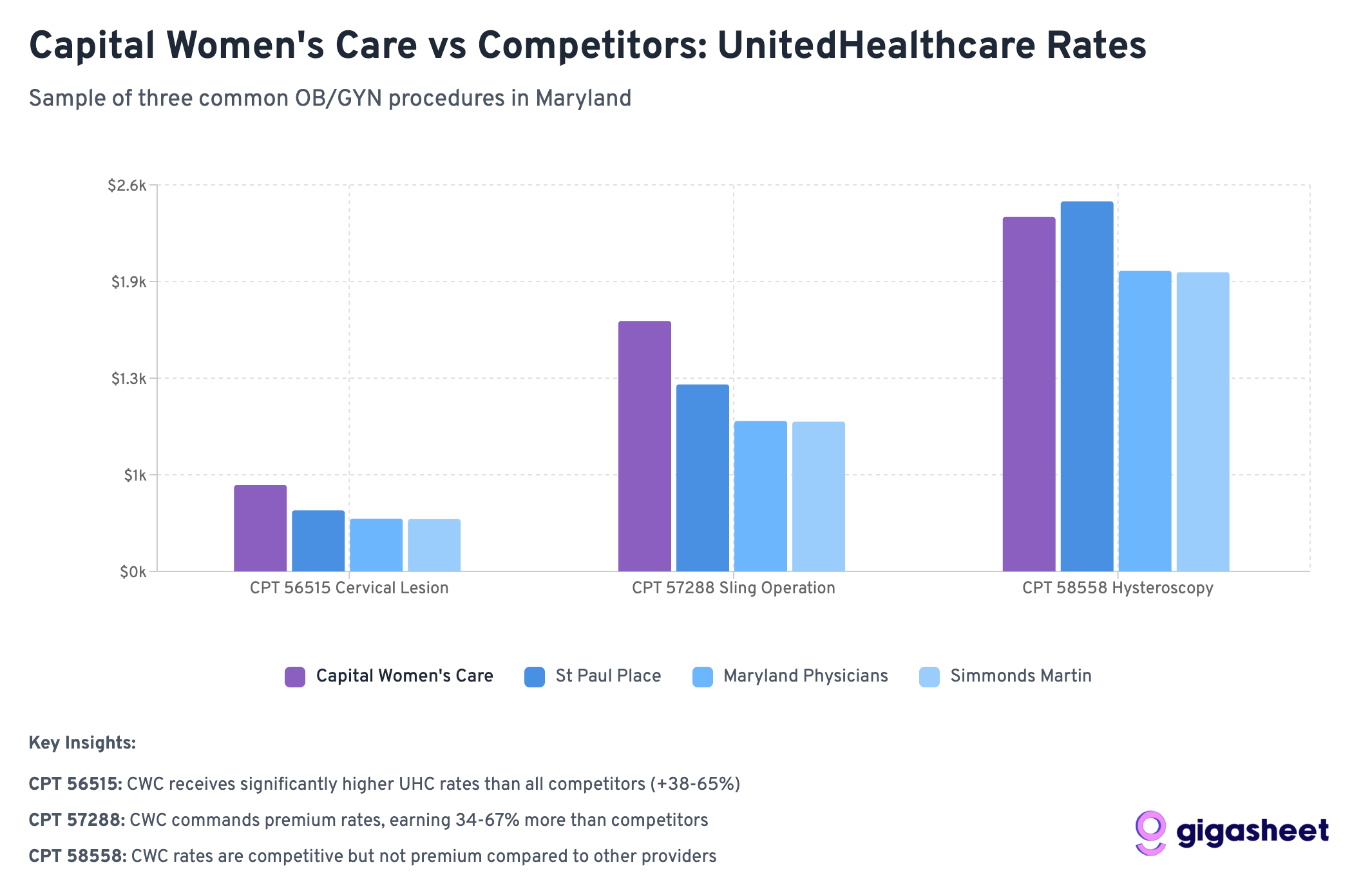

After the analysis in Part 1, we examined the negotiated rates for three common gynecological procedures:

- Code 56515: Destruction of cervical lesions (treatment after abnormal pap smear)

- Code 57288: Sling operation for stress urinary incontinence (surgical procedure)

- Code 58558: Hysteroscopy with sampling (diagnostic procedures for abnormal bleeding)

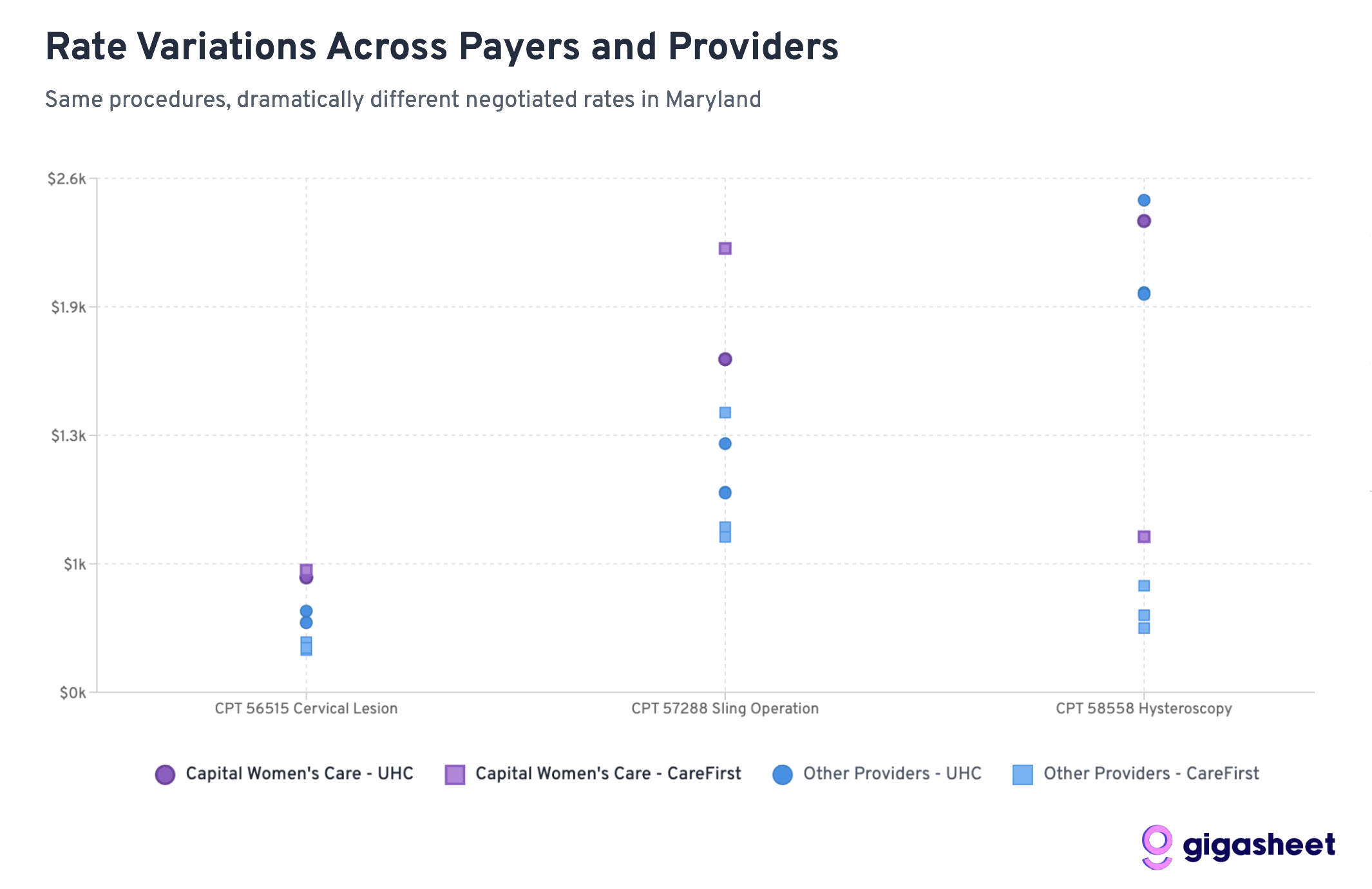

Rate comparison: UHC vs Carefirst

Interest rate changes in price transparency data show a complex competitive landscape where hysteroscopy for UHC is 200-500% higher than that of Carefirs’ payments of 200-500% while secondary attitudes of capital women caregivers show mixed positioning. Sometimes Capital Women Care Orders receive premiums from UHC (code 56515, 57288), while other times they receive comparable rates to smaller competitors (code 58558). The data show that both parties in the CWC-UHC dispute have reasonable arguments: The CWC has received competitive or advanced compensation, and inconsistent rates across procedures indicate room for negotiation.

Main discovery: The story of two insurance strategies

UHC usually pays more than Carefirst

Of the 12 provider production portfolio, UnitedHealthCare pays more than 75% of Carefirst. This shows that Carefirst is more aggressive in negotiating interest rates in the lower Maryland market.

Hysteroscopy shows the biggest difference

For code 58558 (hysteroscopy with sampling), the rate difference was surprising:

- UHC Payment More than 203-519% More care than all providers

- Average UHC rate: ~$2,200 vs Carefirt rate: ~$510

- This represents the biggest system difference throughout the process

Capital Women's Nursing Command Premium Rate

The ratio of CWC to competitors reveals why UHC may resist further increase:

- Code 58558: Despite its large size, CWC's UHC rate ($2,384) is already comparable to its competitors

- Code 56515: CWC gets better terms from UHC ($581) vs. competitors ($352-411)

- Code 57288: CWC obtains significantly higher interest rates from UHC ($1,685) with most competitors ($1,008-1,258).

Width variation

The most extreme example is: Simmonds Martin & Helmbrecht gets 519% of the times from UHC, rather than Carefirst for hysteroscopy procedures (the difference is close to $1,700 per procedure). These patterns suggest that while some programs have established market prices, others (especially diagnostic procedures such as diagnostic mirrors) lack standard pricing, which helps provider-insurer negotiations in complexity, such as CWC-UHC disputes.

What does this mean for the CWC-UHC dispute

CWC has ordered premium

The data reveals a key insight: Capital women’s care does not necessarily receive unfair treatment from UHC. In fact, CWC usually receives higher interest rates than competitors of both insurance companies:

- For hysteroscopy (58558), despite theoretically less negotiation leverage, CWC achieved comparable UHC rates

- For cervical procedures (56515), CWC obtains a 40-65% rate from UHC compared to smaller competitors

- For sling operation (57288), CWC's UHC rate ($1,685) is significantly higher than most competitors

This pattern suggests that UHC's resistance to further growth may be economically rational rather than punitive.

Interest rate split across the industry

The huge difference between UHC and Carefirt rates for all providers highlights the basic pricing inefficient in healthcare. However, in every insurance company's network, the CWC always commands premium rates, which indicates that its market position is already strong.

Proportion and negotiation capabilities

The traditional view shows that larger practices should achieve lower rate per unit due to quantitative efficiency. The data suggests the contrary: CWCs usually get higher interest rates than smaller competitors, which suggests they have successfully used their size to get premium pricing, rather than quantity discounts.

Broader market dynamics

The market power of Carefirst

Carefirst Bluecross BlueShield appears to be using its position as a major insurer in Maryland to significantly reduce the overall negotiations. With a market share of about 50% in Maryland, Carefirst can bargain even more with providers who can’t lose half of their potential patient base.

UHC's perspective becomes clearer

UnitedHealthCare's position in the dispute gains context when the ratio is observed to competitors. UHC has paid the CWC premium rate compared to other OBGYN providers in Maryland. From a UHC perspective, further growth rates will create a larger gap between the CWC they pay for and the smaller practices.

Economics of provider merger

The data illustrates the key tensions in healthcare integration: Large practices believe that the scale is reasonable due to quality and convenience, while insurance companies are concerned about paying premium prices for goods and services. The CWC seems to have successfully established premium pricing, making UHC's resistance economically understandable.

Outlook: What this means for medical expenses

Price transparency revolution

This analysis is simply because federal price transparency requirements come into effect in 2021. For the first time, we can see exactly which insurers pay different providers for the same service, revealing a lot of hidden changes in our healthcare system.

Market efficiency issues

The data raises basic questions about market efficiency:

- Why does the same procedure differ between 500% between insurance companies of the same provider?

- Will patients get better care when insurance companies pay more, or do some insurance companies just pay exaggerated rates?

- How do patients make informed decisions when the ratio changes at the extreme?

Regulatory meaning

These findings may attract regulatory concerns, especially around:

- Is the rate change achieved any legal purpose

- How to ensure patients are not punished for insurance rate disputes

- Price transparency alone is enough to improve market efficiency

Conclusion: Both sides have valid arguments

Capital Women's Care contract dispute with UnitedHealthCare becomes even more nuanced when viewed through competitive interest rate data. Our analysis shows that both parties can point out legitimate evidence supporting their position:

Capital Women's Care's case:

- Inconsistent rates: For some procedures (such as hysteroscopy (58558)), CWC still gets a similar UHC rate to smaller competitors despite the larger size and presumably higher overhead.

- Carefirst comparison: CWC's rates for certain programs obtained from Carefirst are significantly higher (e.g., sling operation is $2,245, while UHC's $1,685) suggest that the room with increased UHC's interest rate exists.

- Reasons for market location:As the largest OBGYN practice in Maryland, CWC can argue their size, convenience and comprehensive service guarantee premium compensation.

UnitedHealthCare case:

- Already premium: In multiple programs, the rate of CWC obtained from UHC is higher than that of smaller competitors (40-65% higher for cervical procedures), indicating that UHC has identified the value of CWC.

- Economic rationality: Further growth rates will create a larger premium gap between CWC and other providers, which may make UHC's cyber economics unsustainable.

- Hybrid performance: The inconsistent pattern across programs shows that the premium positioning of CWC is inconsistent across all services.

Complexity of medical negotiation:

This data is not a clear case of unfair treatment, but reveals the inherent complexity of health care rate negotiations. Both parties can legitimately point out specific procedures and compare situations that support their position, while the overall situation remains a true mix.

The analysis shows that the dispute reflects a broader challenge in healthcare pricing: how do you fairly compensate for size and market position while maintaining a reasonable cost structure? Competitive data indicate that there is no obvious “correct” answer. Just a different approach to explaining the same complex market dynamics.

The real insight is not that one party is obviously correct, but that negotiations on health care rates involve legitimate competitive interests, allowing reasonable people to view the same data and draw different conclusions on fair pay.

Jason Hines is the CEO of Gigasheet, which provides AI-driven price transparency market intelligence.

notes: The analysis is based on a sample of price transparency data submitted by UnitedHealthCare and Carefirst Bluecross Bluecross bluecross as stipulated by federal regulations. Rate calculation is a summary of data for multiple contracts and locations within each provider organization. To expand interest rate analysis from Part 1, we use a public data source to resolve EINS to organization names.