How much will your long-term care cost? It Depends on Your Average – Center for Retirement Research

Consulting firm Milliman recently released its 2025 Long-Term Care Index, which calculated that, on average, a 65-year-old should set aside $135,000 for future intensive long-term care needs.

great changes

While average numbers may be a useful anchor, Milliman's estimates show wide variation based on factors such as gender, location and health status. For example, the average cost for women is $171,000 and for men is $98,000, mainly because women live longer. As a result, they may need care for longer periods of time and are less likely to have a spouse to help them for free.

According to Milliman, almost half of men and four in 10 women require no paid care at all during their lifetime. Another quarter of men will receive paid care for less than a year, and only 29% will need paid care for more than a year. Women, on the other hand, are more likely to need long-term care, with 41% facing care for more than a year and 14% for five years or more, which will cost them an average of $665,000 (see Figure 1).

I should point out that Milliman's data assumes that all care is Salary care. The Center for Retirement Research at Boston College estimates that families typically provide at least half of the caregiving time, even for people with high needs. Milliman also did not disclose how those costs were paid, specifically whether they included Medicaid-covered care or just out-of-pocket costs.

location, location, location

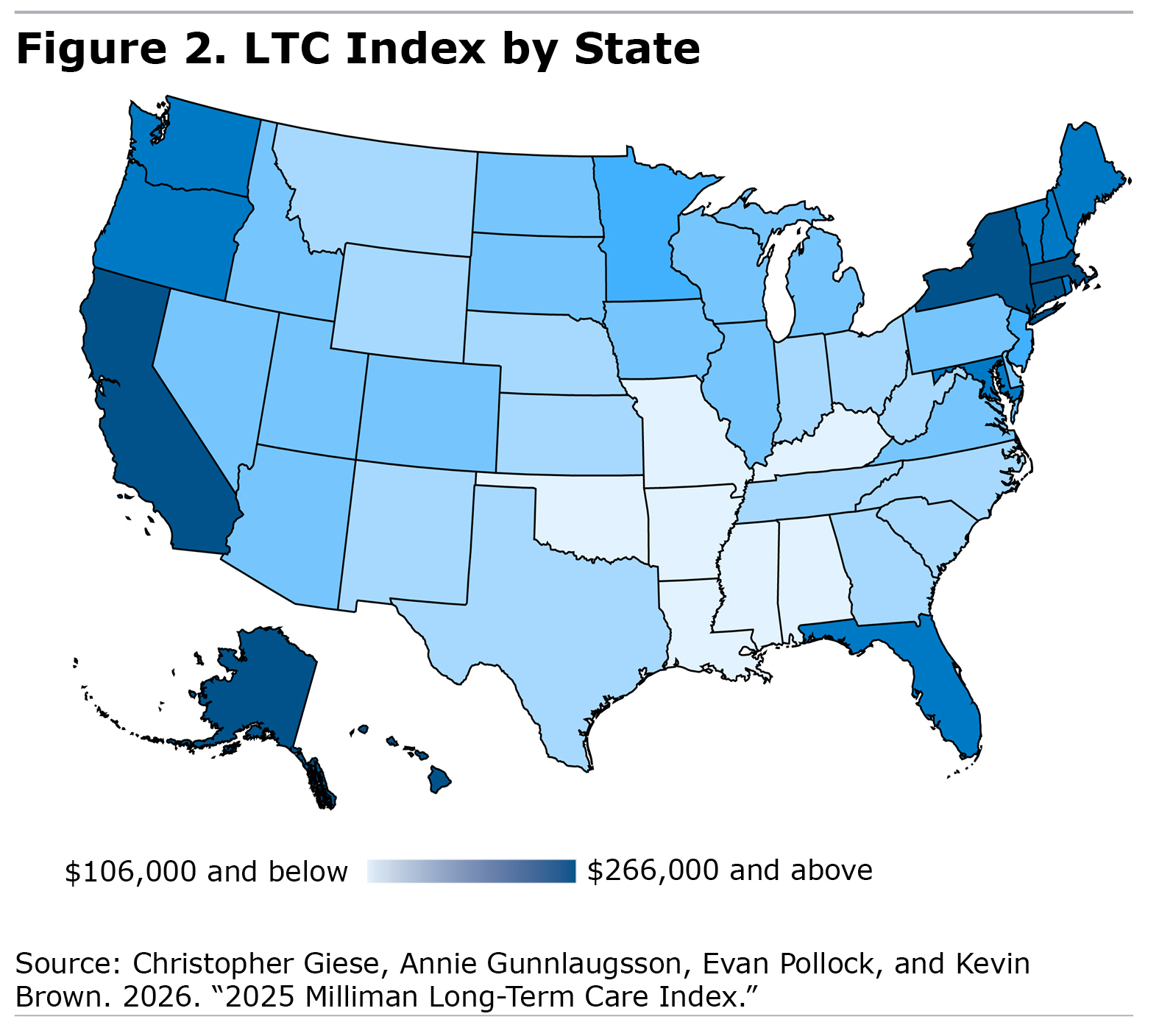

Costs vary widely depending on the type of care needed (home health, assisted living, or nursing home) and location. Location is not only related to the cost of care, but also to longevity and health. In some states, such as Hawaii, California, Washington, Florida, and New Hampshire, people live longer (and therefore may need care for longer) than in other states, such as Mississippi, Alabama, West Virginia, Louisiana, and Kentucky.

On the other hand, healthier people tend to require less time for care. Milliman highlighted Colorado, Montana and Hawaii as states where residents are least likely to need any paid long-term care, and Montana, Arizona and Oklahoma as states where people need care for the shortest amount of time. On the other hand, people with care needs took the longest to receive care in Hawaii, Connecticut and New York.

Taking all of these factors into account, taking into account the cost of long-term care services, the likelihood of needing services, and the duration of need, Figure 2 shows Milliman's ranking of the average long-term care costs in each state (see Figure 2).

The most expensive states (dark blue) are on the West Coast and Northeast, where the average cost is about twice the national average. The cheapest are mainly in the south-central region (light blue).

Another change in how much money a 65-year-old needs to set aside for his or her own care is the expected rate of return. The average return on investment of $135,000 is 4.35%. Using the higher figure of 7%, the average 65-year-old would only have to set aside $74,000, but using the lower rate of return of 3%, they would need to have $187,000 in the bank.

What does this mean to you?

For individuals and families planning for future long-term care expenses, predicting needs can be difficult. I've written before about factors that influence the need for paid long-term care, including overall health, family history, and family circumstances.

But the $135,000 figure seems like a good starting point. Increase that number if you live in a high-cost state, have a family history of dementia or other conditions that may require long-term help, or if you don't have family members who can help.

Your existing health conditions can affect this number both positively and negatively. If you already have a debilitating, chronic disease that may stay with you for years, such as Parkinson's disease, you may need more money. But if you have a type of cancer that may shorten your life but won't cause long-term disability, your needs may be much less.

Insurance solution?

My biggest takeaway from the Milliman report is that we need a universal long-term care insurance program because we have so much uncertainty about individual needs and relative certainty about the needs of the elderly population as a whole. Furthermore, while a small percentage of older adults can afford care, the majority cannot.

According to the Federal Reserve, the median retirement savings for Americans ages 65 to 74 is $200,000, meaning half have less than that amount. The median personal savings for those over 75 is just $130,000. In short, most baby boomers may not have enough money to pay for long-term care in the future.

If we started paying into the national insurance scheme at an earlier age, the cost of meeting long-term care needs would be significantly reduced. Milliman calculated that at a 4.35 percent return, a 35-year-old would have to set aside an average of just $38,000 to pay for future long-term care expenses, nearly $100,000 less than a 65-year-old. Of course, few 35-year-olds are thinking about their future care needs, but together we can meet this challenge. In fact, Washington state already has such a program to provide its workers with basic long-term care protection (up to $36,500); it is also exploring ways to allow people to purchase additional long-term care coverage at group rates. Several other states, including Massachusetts, are already exploring similar plans.

For more information about Harry Margolis, check out his Adventures in Aging in America blog and podcast. He also answers consumer estate planning questions on AskHarry.info. To stay up to date with the Squared Away blog, join our free email list.