Price transparency data reveals the true story behind Capital Women’s Care and UnitedHealthCare Contract Battle (Part 1) – Healthcare Blog

– Healthcare Blog")

Jason Hines

On August 1, 2025, Capital Women's Care (CWC), one of the largest OB/GYN practices in the Mid-Atlantic region went out-of-network with UnitedHealthcare, affecting tens of thousands of women across Maryland, Virginia, Pennsylvania, and Washington DC The contract dispute between Capital Women's Care (CWC) and UnitedHealthcare offers a fascinating case study in how price transparency data can illuminate the real dynamics behind these high-risk negotiations.

Public combat

Capital Women’s Care, which has more than 250 doctors and healthcare professionals, confirmed that its agreement with UnitedHealthcare will fail despite negotiations. The practice urges patients to contact UHC to express their concerns about losing access to providers.

UnitedHealthCare fired on its website with a detailed public claim, accusing the CWC of “refusing to get rid of the double-digit price increase” and “costs are much higher today than its peer providers in Maryland and Virginia.” UHC provides specific examples claiming that vaginal delivery costs of CWC are more than 120% higher, or $2,600 more, compared to the average cost of other OB/GYN providers”.

But what does the actual price transparency data on these competing claims reveal?

What is displayed in transparency data

Using Capital Women’s Care to negotiate rates from UnitedHealthCare’s own machine-readable files, we analyzed samples of common OB/GYN program for Maryland interest rate data. While this represents only part of all the procedures and is specifically targeting rates in Maryland, it provides valuable insight into the real payment dynamics between these organizations. These data are nuanced than any party’s public statement suggests.

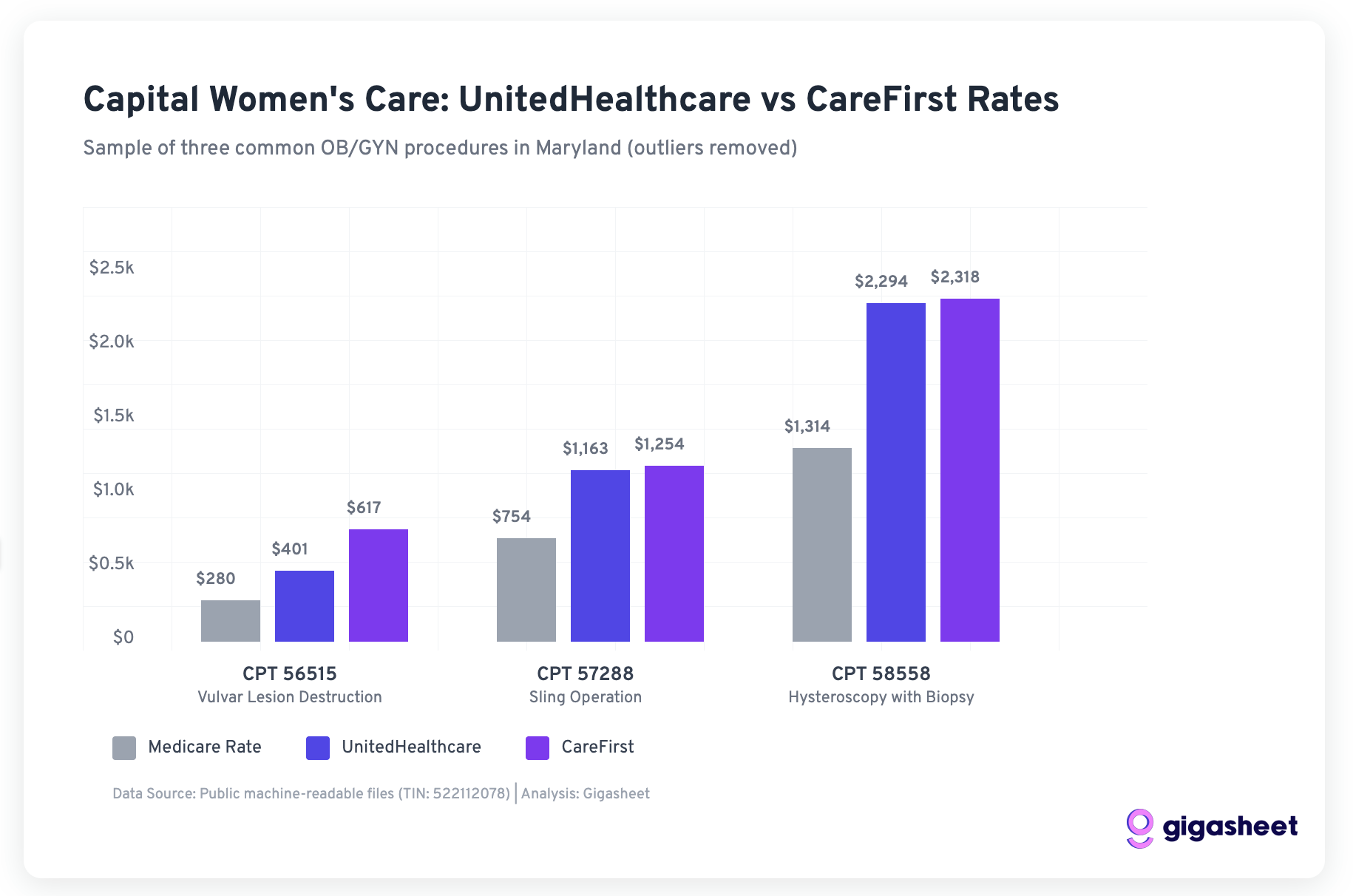

Data Methodology Note: Our analysis examines the cost of capital women’s care negotiated from publicly readable machine-readable files, focusing on Maryland providers and filtering out statistical outliers (ratio below 500% or above 500% of Medicare). We analyzed the interest rates for UnitedHealthCare and Carefirst for three common OB/GYN programs, in which both payers had sufficient data.

CWC's interest rate positions with other payers

Our analysis of three common OB/GYN programs in Maryland shows that the ratio of CWC to UnitedHealthCare is actually quite competitive compared to other major payers:

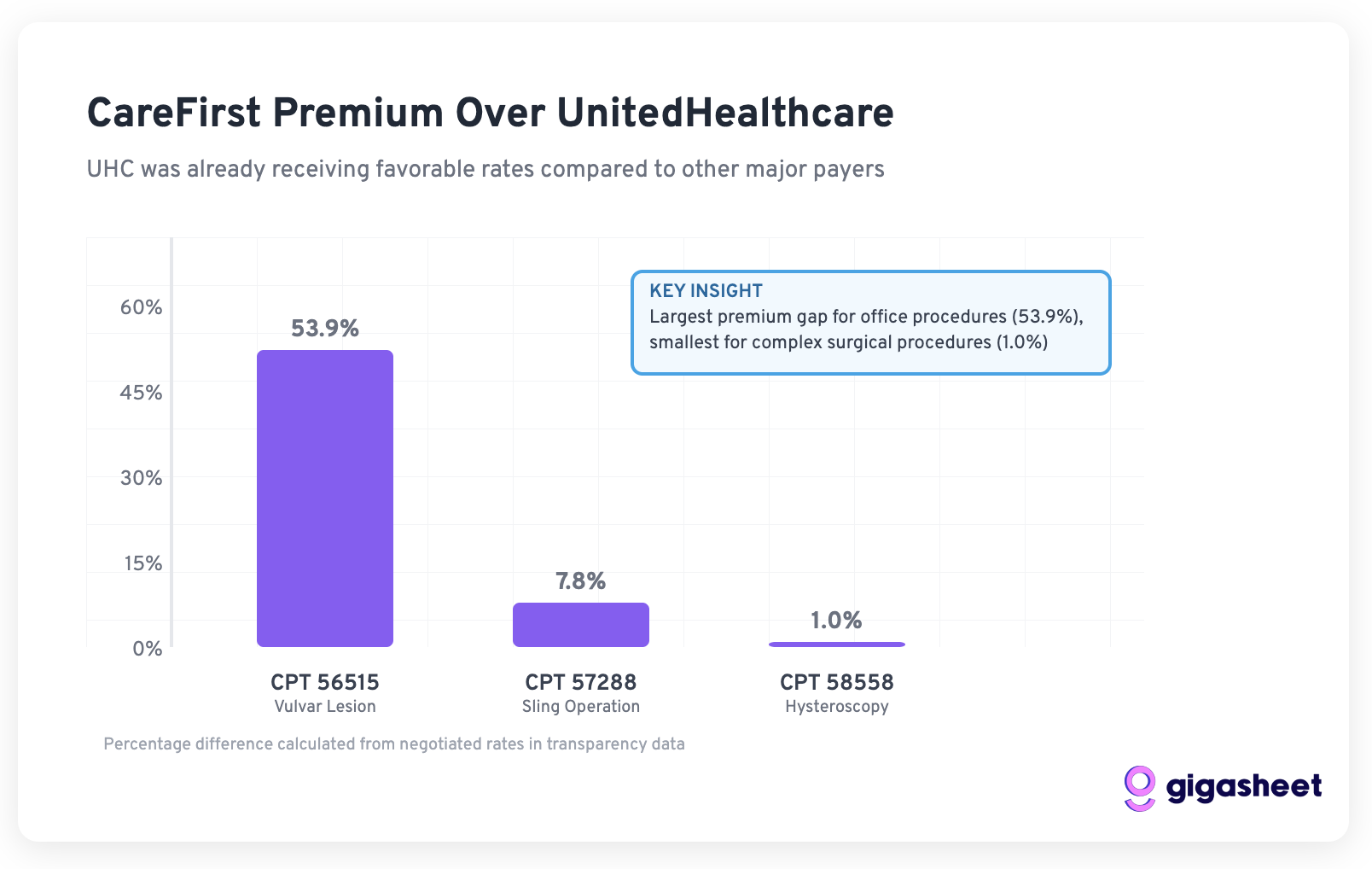

For three procedures that both UHC and Carefirst negotiate with CWC:

- CPT 56515 (Vulvar lesions destruction): UHC paid $401 vs Carefirst $617 (53.9% difference)

- CPT 57288 (Sling Operation): UHC paid $1,163 vs Carefirst $1,254 (7.8% difference)

- CPT 58558 (Hysteroscopy): UHC paid $2,294 vs Carefirst $2,318 (1.0% difference)

The sample data suggests that UN Health has already obtained favorable interest rates from the CWC compared to other major payers, a questioning UHC’s claim about CWC is “more costly.”

Medicare benchmark reality

UHC and Carefirst pay much more than Medicare in our sample:

- UnitedHealthCare: 143-175% Medicare premium rate

- Carefirst: 166-220% Medicare premium rate

Although Carefirst pays higher rates, UnitedHealthCare's interest rate remains a large premium reimbursement by the government, suggesting that the “double-digit increase” required by the CWC may be an attempt to align with the market interest rates other payers are willing to pay.

Important limitations: The analysis is based only on samples from three programs in Maryland. A comprehensive analysis will require examining CWC operations to fully validate all program codes in all markets of these models.

Strategic background: Market share is important

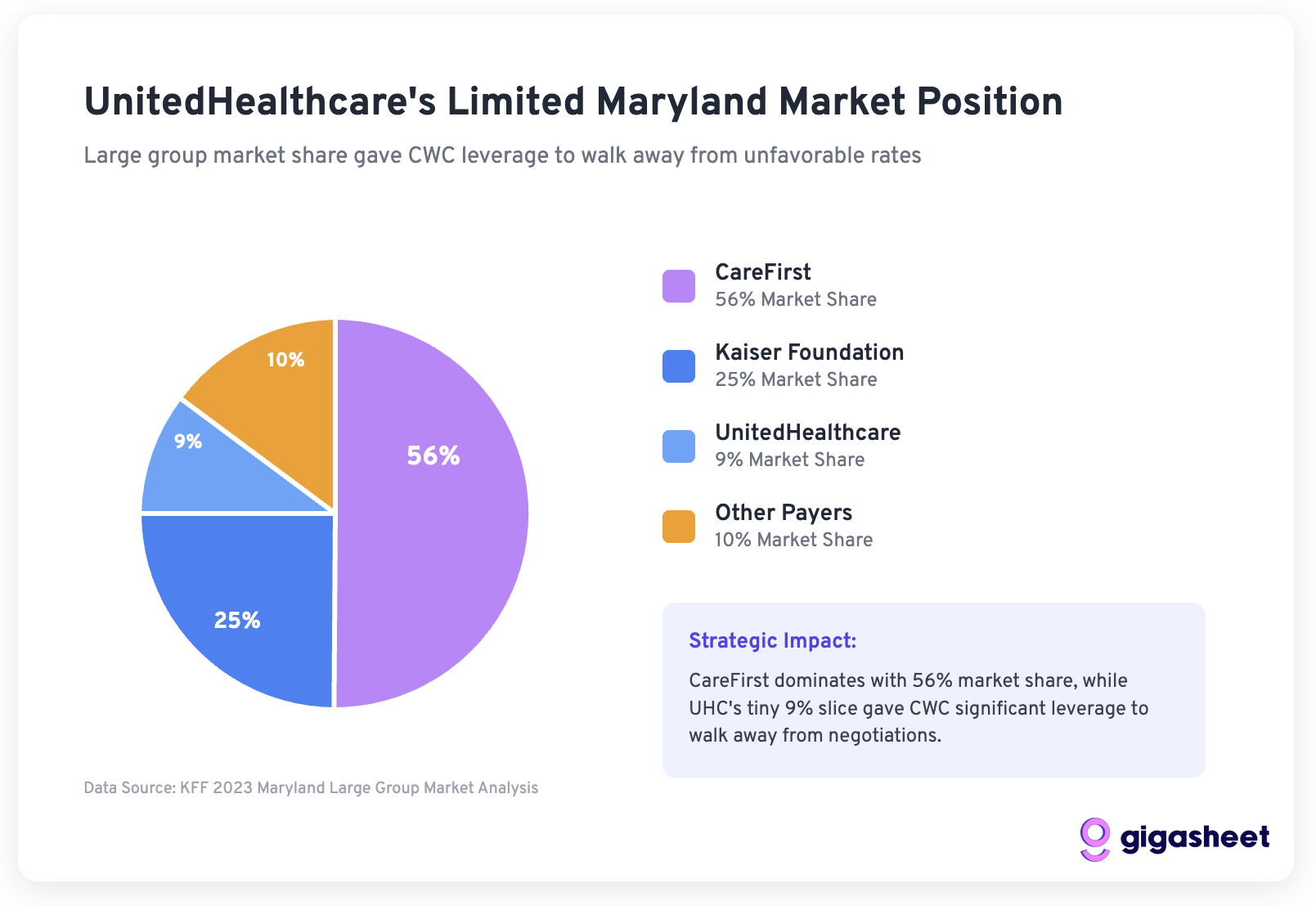

To understand why CWC may go away, you need to check UnitedHealthCare's position in the Maryland market. According to KFF data, UnitedHealthCare accounts for only 9% of the large-scale market share in Maryland as of 2023. This relatively small market position has brought huge leverage to CWC.

Mathematics to walk away:

- UHC represents a small part of the basis of CWC patients

- CWC signs a contract with a larger payer (Aetna, Carefirst, Cigna) to pay higher rates

- This practice serves more than 250 providers in multiple states

- Leaving 9% of the market to establish a precedent is strategic

Evaluate UnitedHealthCare's public claims

UHC's website has made some specific claims that we can evaluate based on transparency data:

1: “CWC is much more costly than peer providers”

Assessment: Partially misleading

Although CWC may charge more than some providers, our analysis shows that UHC pays competitive rates compared to other major payers. “Peer providers” lack background on the differences in geographical market prices and provider quality.

2: “Double-digit prices rise, which will make them 30% higher than the average average”

Assessment: Missing background

The claim is not specified:

- How is UHC's current interest rate compared to other payers

- Does the “average” include lower quality or different positioning providers

- Regional cost changes in expensive Mid-Atlantic markets

3. Comparison of specific program costs

Assessment: Potentially accurate but incomplete

UHC’s claims on delivery costs may be accurate, but they do not provide a complete market environment. Transparency data show significant rate changes between payer and program, indicating that “expensive” is relative to the selected comparison set.

How price transparency changes the game

This controversy illustrates how price transparency data can reshape medical negotiations in a variety of ways:

Informed leverage

Providers like CWC can now see exactly how their rates compare between payers, enabling more strategic negotiations. CWC knows that they are giving UHC a favorable price compared to Carefirst.

Public Accountability

Both parties filed public claims and fact checks can now be conducted based on the actual negotiated interest rates. UHC’s statement about CWC “costs more” is more nuanced when opposing the full payer landscape.

Market benchmarking

Transparency data display:

- There are big differences in regional markets

- Provider quality and market position prove that interest rate premiums are reasonable

- “Expensive” is relative to making comparisons

Strategic positioning

For the practice of CWC market position, it is crucial to maintain the interest rate discipline of payers. Accepting a payer's lower than the market rate can disrupt negotiations with others.

The real winner: market transparency

Although patients are captured in the middle of this dispute, the broader health care market benefits from the transparency provided by this conflict. The public availability of actual negotiated rates means:

- patient Make smarter choices about providers and plans

- employer A better evaluation of insurance plan value propositions

- Provider Its interest rates can be benchmarked based on actual market data

- Payer Interest rate decisions that use real data rather than selective comparisons must be justified

Outlook: Lessons from medical negotiations

The CWC-UHC dispute offers several lessons for future health care contract negotiations:

- Price transparency data is now a negotiation tool – Both parties can and will use actual rate comparisons to support their position

- Market share in terms of rate negotiation – UHC's 9% Maryland market share limits its leverage

- Public relations war requires data support – Claims about “expensive” providers can now be fact checked with the actual negotiated rates

- Provider merger creates negotiation power – Large practices like CWC can't afford a contract

The solution

Regarding this specific dispute, the transparency data shows that both parties have reasonable positions:

- CWC Compared to other payers, it does give UHC a favorable interest rate, demonstrating their increased requirements

- UHC Facing pressure to control member costs while maintaining adequate provider networks

Resolutions may require:

- UHC admits that they are currently at a lower price than the market

- CWC acceptance rate of sharp increase affects patient costs

- Both sides find a middle-level position that reflects the true market positioning

In theory, the availability of actually negotiated interest rate data should increase the productivity of these conversations by establishing common facts about market interest rates and provider positioning.

in conclusion

Capital Women's Care contract dispute with UnitedHealthCare shows that price transparency fundamentally changes health care negotiations. Although both sides have made public claims in favor of their position, our analysis of interest rate data actually negotiated in Maryland reveals a more complex story in which market dynamics, strategic positioning and regional factors all play a crucial role.

Key points of our data analysis:

- UHC pays competitive interest rates compared to other major payers compared to the procedures we checked

- Given UHC's limited 9% Maryland market share, it's strategic to make a decision to go away

- Both payers are paying higher than Medicare rates, suggesting room for negotiation

Important warning: Our analysis examines only three common procedures for Maryland data. A comprehensive assessment will require analyzing CWC operations to fully validate all program codes on all markets for these models.

As more and more stakeholders have access to this previously hidden pricing information, we can expect healthcare contract negotiations to become more data-driven, transparent, and ultimately more reasonable. The real winners will be those who can effectively analyze and take this new transparency to better determine health insurance, provider choices and contract terms.

I'll go back to THCB to see the rest of the background of the dispute in Part 2. What are the costs of these services?

Jason Hines is the CEO of Gigasheet, which provides AI-driven price transparency market intelligence.